How to Deduct Stock Losses From Your Tax Bill

Aug 15, 2024 By Rick Novak

Are you one of the many stock market investors who have seen their investments dive

recently? If so, you’re not alone, the volatility that has been rampant in the markets this year has impacted nearly every investor.

However, instead of feeling completely powerless in the face of these market forces, there is a way to use losses to lower your tax bill. In this blog post, we're going to discuss how deductions for capital losses can be used as a tool to reduce your taxes owed and save money.

A Guide to Understanding the Basics of Tax Loss Harvesting

Tax loss harvesting is a tax-saving strategy in which you sell investments that have decreased in value and use the losses to reduce your taxable income. The benefit of this method is that losses can be used to offset other capital gains, such as those from winning stocks or investments outside of the stock market.

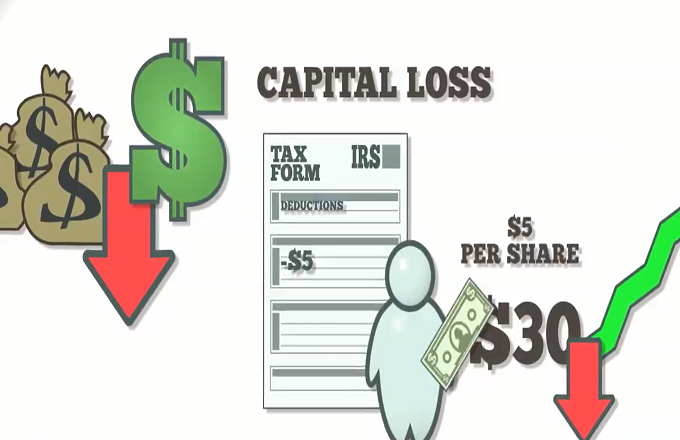

Understanding Stock Losses

Stock losses occur when the price of a security drops below its purchase price. For example, if you bought 100 shares for $10 per share and the current value falls to $8 per share, your loss would be $200 ($2 x 100 = $200). When this happens, it’s important to understand that you can only deduct stock losses in the year that they occur.

Determining Capital Losses

To properly calculate your capital loss, you’ll need to determine two important figures: the purchase price and sale prices. The purchase price should be the average of all prices paid for security over time, including commission fees.

On the other hand, the sale price should include any additional costs such as broker fees or taxes. Once you have these two figures, you can subtract the purchase price from the sale price to determine your capital loss.

Capital Loss Deduction Rules

There are some important rules to keep in mind when it comes to deducting stock losses for tax purposes. First, capital losses must be used to offset any gains before being deducted from your taxable income.

That means if you have a $2,000 capital gain and a $1,200 capital loss in the same tax year, you can only deduct up to $2,000 of your losses. Additionally, if your total losses exceed your annual gains, you can only deduct up to $3,000 from your taxable income.

Deducting Capital Losses

Now that you understand the rules for deducting capital losses, it’s time to take advantage of this tax break. To do so, simply subtract your total yearly losses from your taxable income when filing your taxes.

This will reduce your final tax bill and help you save money in the long run. Deducing capital losses can be a great way to offset the impact of market volatility and reduce your overall tax burden.

Common Mistakes With Reporting Stock Losses - What You Should Know

When it comes to reporting stock losses for tax purposes, investors make a few common mistakes. First, many investors need to remember to include the purchase price of a security in their calculations, which can result in an inaccurate deduction amount.

Additionally, some investors need to factor in commissions and fees when calculating the sale price of a security. Lastly, some investors must consider the maximum deduction limits and accidentally over-deduct their losses.

To avoid making these types of mistakes, it’s important to double-check your calculations before filing for deductions. Additionally, you should consult a tax professional if you need help understanding the rules or calculating your deductions.

Exploring the Different Types of Stock Losses and How To Deduct Them

There are two main types of stock losses that you can deduct from your taxes: short-term losses and long-term losses. Short-term losses occur when a security is held for less than one year, while long-term losses occur when a security is held for more than one year.

short-term losses

It can be deducted in full, while long-term losses are subject to certain limits.

Another important aspect of deducting stock losses is understanding the rules for net capital loss carryovers.

Long-term losses

It can be carried over for up to three years, allowing you to deduct the loss in future tax years.

By understanding these rules and taking advantage of stock loss deductions, you can save money on your taxes, make wiser investment decisions, and take action to minimize your risk of stock losses.

Tax Loss Carryovers

Tax loss carryovers can be a great way to reduce your taxable income and save money on taxes. When you have an unrealized capital gain or a net capital loss in any given year, the number of your losses can be “carried over” into future tax years. This means that you can use the excess losses to offset

FAQs

Can you offset stock losses against income tax?

Yes, you can offset stock losses against your income tax. This is done by subtracting the total capital loss from any capital gains you have made in the same tax year. Any excess losses can also be carried over to future tax years.

Are stock losses deductible?

Yes, stock losses can be deducted from your taxes if you follow the capital gains and losses rules. This includes deducting any losses against your total gains before being deducted from your taxable income and understanding the limits for how much can be deducted each year.

What is a capital loss carryover?

A capital loss carryover occurs when an investor has an unrealized capital gain or net capital loss in a given year. The amount of the losses can be “carried over” into future tax years, allowing the investor to use the excess losses to offset gains in later years.

Conclusion

Understanding how to report stock losses and take advantage of capital loss carryovers can be a great way to save money on your taxes. By following the rules for capital gains and losses, you can deduct any losses from your total gains before subtracting them from your taxable income when filing your taxes.

By understanding the rules for net capital loss carryovers, you can take advantage of the savings opportunities that come with carrying over losses into future years. With some smart planning and knowledge of the rules, you can maximize your deductions and increase your savings.

How to Use Venmo and How It Compares to Competitors: Everything You Need to Know

Teen Tax Essentials: Empowering Financial Literacy

Learning the Art of Showing Your House to Buyers

How Much Money Can Day Traders Make?

How to Create a Cash Flow Projection for Your Business: A Step-by-Step Guide

At What Age Does Car Insurance Go Down? Types of Coverage

Should You Cash in Your Pension? 5 Important Things to Consider

Understanding Credit Card Cash Advances

Bank Fees You Should Never Have to Pay: A Comprehensive Guide